Please fill out the details below to receive information on Blue Wealth Events

"*" indicates required fields

Housing affordability. If only you hadn’t had that smashed avo, quinoa and organic coke, you’d be living in a waterfront in Rose Bay. At least a heap of the commentary makes it seem that way. The problem with statements like these is that they often dominate affordability discourse at the expense of getting to the facts and providing real solutions.

I completely understand that getting into the property market, particularly for a young Sydneysider, can seem daunting. I also understand that Sydney isn’t the only city in Australia. Much like how Galileo had to convince his peers (unsuccessfully) that earth wasn’t at the centre of the universe, it’s time we let property market commentators know that Sydney isn’t the centre of the property universe.

I digress. There are two components of affordability:

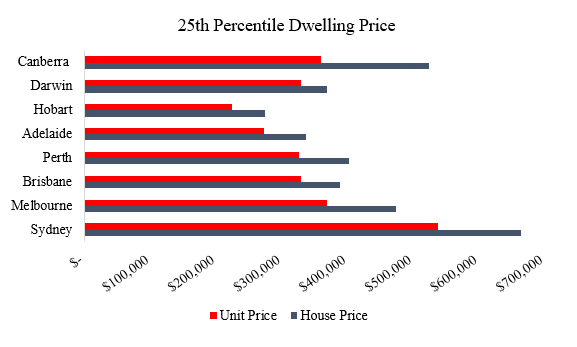

I touched on point two a few weeks ago, so today I’ll discuss the cost of entry. Rather than look at the median priced property in each city, let’s focus our attention on young Australians and look at a more affordable option. The figure below shows the 25th percentile house and apartment prices in each of our capital cities. If there were 100 property sales sorted cheapest to most expensive, the 25th percentile property would be the 25th most expensive of the sample.

For brevity let’s focus on housing in Sydney, Melbourne and Brisbane. Distance to CBD measures the minimum kilometres you’d need to go out to buy a property of the price in column two:

The average house 60 kilometres from Sydney’s CBD is 40% more expensive than one 25 kilometres from Melbourne’s CBD and 70% more expensive than one 30 kilometres from Brisbane’s CBD. Seems less daunting now, doesn’t it?

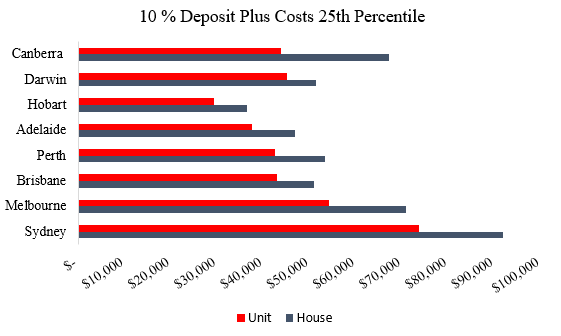

The figure below shows how much you’d need to save to buy the 25th percentile property in our capital cities. Figures are based on:

The figures don’t include lender’s mortgage insurance (LMI). LMI can be paid up front or capitalised into the loan repayments and will result in marginally higher mortgage repayments or a larger up-front deposit.

For that 25th percentile house, the cost of entry in Sydney is 30% higher than in Melbourne and 80% higher than in Brisbane. By investing outside of Sydney, you can get your money working for you sooner and avoid what will likely be a few years where Sydney prices move sideways as opposed to upward.

My message to young Australians is get educated, develop a plan and take action … and, of course, don’t eat out. Ever!