Please fill out the details below to receive information on Blue Wealth Events

"*" indicates required fields

In the past few weeks, I’ve been asked many times what I believe will happen to the property market as a result of the impact of COVID-19. This is a summary of my thoughts.

We know COVID-19 has impacted a lot of industries and impacted people’s decision-making. For us, our focus is always trying to understand property markets and how the environment of the moment impacts on that market. Of course, we know that when the environment at the time is positive, it impacts on the market positively and when the environment of the time is not so positive it might have a negative or minimal influence on it.

COVID-19 is unprecedented. It’s like nothing we’ve ever seen before. We’ve lived through a few dramas in recent decades; the Global Financial Crisis (GFC), the European debt crisis, before that September 11 and the bursting of the tech bubble, Y2K, the recession we had to have, the 1987 share market crash and a whole bunch of others in between; natural, economic and political.

Forming a clear opinion in this environment and understanding what will happen in the next few months is very difficult. There’s a fair bit of educated guesswork. What we do know, is that the property market to a great extent, like the rest of the economy, has gone into a holding pattern. The word ‘hibernation’ has been thrown around regularly and it feels like the perfect description. What typically affects property markets up or down is supply and demand. A whole bunch of things impact supply (investor confidence, construction, council efficiency, finance, developer confidence) and a whole bunch of things impact demand (population growth, jobs, finance, investor confidence, demographic shifts, infrastructure investment and so on).

The key question most people want answered is whether or not there’ll be a property market crash. While I can’t unequivocally say there won’t be one, I can certainly give you an insight into my thought process around the supply demand balance or imbalance in this period and the likelihood of a crash.

For there to be a property crash there has to be a lot of supply come on to the market very quickly. I’m not saying that’s not going to happen, but I do believe it’s highly unlikely. Why is it highly unlikely? For a couple of reasons. Australians don’t generally abandon their homes in difficult times. History has shown us that. The retention of our homes at all costs is in the fabric of our culture. Aussies hold onto the great Australian dream and do whatever they need to do to hold onto their homes. This is why we have never actually seen a property market crash in Australia (a crash is defined as a 10% annual fall in median prices across the country) – it’s not happened.

Could it happen this time though? Will lots of Australians sell their homes and saturate the market? The only way that might happen is if Australians are forced to sell because of a significant increase in unemployment where millions of Australians lose their jobs in a very short period of time. ‘That’s just happened’ I hear you say. Well, not quite. We know there has been a significant and rapid increase in unemployment, however, the government has moved quickly to shore up employment by introducing the Job Keeper Allowance. The Job Keeper Allowance has already had a significant impact on reducing the number of unemployed people or people being permanently stood down. What we do know is that many businesses have stood down staff on the Job Keeper payments ($1,500 per fortnight). This has a couple of positive impacts. The first is that it significantly improves people’s chances of paying their mortgage, and secondly, when we return to some form of ‘normality’ those businesses will hit the ground running without the need to re-employ and re-train new staff. All of this is very positive for a quicker than expected economic recovery.

There are two other reasons that can’t be ignored, that support the argument that we’re highly unlikely to see a lot of supply come onto the market very quickly. The first is that many Australians are ahead on their mortgages with money in a redraw facility or in an offset account. This is partly a function of the low-interest rates that we’ve enjoyed for many years, along with the increased sophistication of loan products over the past couple of decades. The second is that isolation means less household expenditure. We’re not spending money on holidays, weekends away, drinking sessions at the pub, food and drinks at the footy, kids’ sport, window shopping (as much), dinner parties, birthday parties, weddings gifts, gym memberships, beauty services, and the list goes on and on. Money usually spent living our daily lives is now going into necessary fixed costs of which our mortgage is a top priority. The property industry is protected from mass unemployment as a result of the government initiative around Job Keeper and their rules around isolation.

Now let’s talk about the banks. We’ve established that the only way that there will be a mass supply coming onto the market is if people can’t afford to pay their mortgage. The extended version of that is that when someone doesn’t pay their mortgage for a prolonged period of time, the bank forecloses on them and sells their property to recover the amount of the loan. Two things here. Firstly, assuming people have an income source, either a job or a Job Keeper payment, extremely low-interest rates makes paying our monthly repayments easier. We know that the holding cost of a property, whether it be your home or investment property is lower now than it’s ever been. Interest rates are the lowest they’ve been in our lifetime. Secondly, the banks have clearly shown a willingness to support loan holders through this period. They’ve done this in a few different forms. They have agreed to defer mortgage payments, (some of them) to not charge interest on deferred interest payments and to switch loans from principle and interest (P & I) to interest-only. For someone with a 30-year, $500,000 loan paying 3% interest, the P & I payment would normally be $2,108 per month. The interest-only payment is $1,250 per month; a saving of $858. These are significant factors that will keep the pressure off the market long enough for us to get through this period, and without placing undue pressure on Australians to have to dump their homes by putting them on the market and selling them quickly. Aussies will hibernate in and over their homes for the coming months.

Another key factor is around the supply of new property. What will definitely happen through this period is that there will be a significant reduction in supply of new property. Why? Because like everybody else, developers will go into hibernation; many of them, not all of them. They’ll sit on the development sites they have, they’ll delay the construction they had planned, they’ll delay approaching the bank for funding for their next project. What does this mean? When we do come out of this, people will get their jobs back, they’ll start to go back to work, we’ll start to resume some impression of life before Corona and what we will find is a significant lack of supply in all markets across Australia. That will likely mean an increase in rentals, and also will likely mean an increase in pricing as a result of stable demand or potentially increasing demand. Supply levels are likely to be lower than they were back in the 1950s and 1960s. We saw that post-GFC when Sydney new-property-approval rates fell to 1960s levels. The same dynamics exist here.

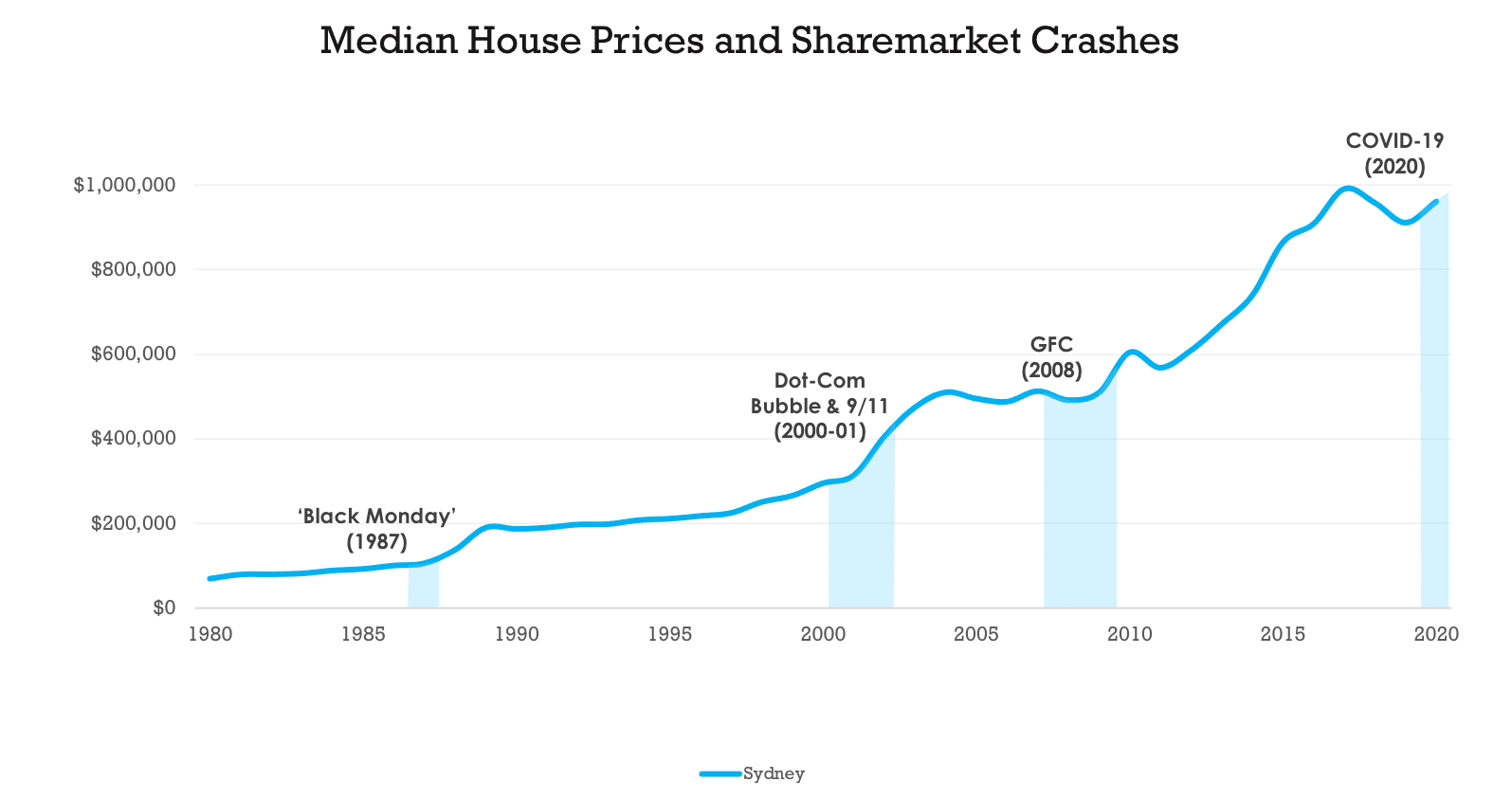

So from my perspective, that’s what we’re likely to see over the next few months. You know history usually gives us some indication of what might happen in the future, even though we know history doesn’t repeat itself exactly. As you can see from the graph below property markets respond well, in some cases very well, to disasters and particularly to share market crashes.

One reason for that, of course, is that most Australians have a significant amount of their superannuation invested in the share market and when the share market cops a beating so does their superannuation. Therefore lots of Australians look for an alternative superannuation investment and many of them turn to property. We saw this post-GFC. I think we might see a repeat of that. We’ll also see Australians moving to property as an alternate investment to the share market whether it be inside or outside superannuation. We’ll see people start to gravitate towards an asset they understand, an asset they are more comfortable with, and that asset is property. Australians will want to put their money somewhere and they want to feel like it’s secure and free of the extreme volatility of the share market. They won’t want to leave it in cash because of the record low returns on cash.

So they’re my thoughts. Only time will tell whether what I’m thinking will come to pass. What we do know is that this period will pass and property will resume some sort of normality with people buying, selling and renting. We know we were coming into a low supply period before this all started and this current period will only exacerbate that low supply. Low supply in markets usually means pressure on pricing and rentals. We’ll see what kind of impact that places on prices and rents this time around.

I’ll leave you with a bit of psychology. When this passes, people will want to make up for lost time. We’ll behave like caged animals released into the wild. Social media is full of posts about what people want to do when they’re ‘released’ from isolation – holidays, catch-ups, dinner parties and delayed celebrations. We will explode out of the blocks and that will stimulate spending and further secure people’s employment.

In the meantime, don’t panic and find the silver lining. Life is what you make it. This will pass.

TH