Please fill out the details below to receive information on Blue Wealth Events

"*" indicates required fields

Most people that have been to one of our seminars would have seen the stats about the proportion of Australians that own more than one investment property.

Only 2.5% of the population owns more than one investment property so if you’re in this group already, congratulations!

Overall, 8.8% of Australians own investment property. Of those 6.3% own one, 1.7% own two, 0.52% own three, 0.21% own four, 0.08% own five and 0.09% own six or more.

For many people, the aim of owning investment property is to provide a passive income for retirement. There are many ways to go about this, but ultimately all of them can all be distilled down to deploying the capital that you’ve built up over your working life into some kind of income generating asset.

It’s important to keep in mind that the market offers many types of properties but they can roughly be separated into:

At present the highest yields which can be found in typical residential investment properties in the safer markets close to metropolitan areas are around 7% – this is mostly limited to dual occupancy types. The lowest would be around the 2.5-3% mark for typical investment properties. Luxury property while usually having very high rates of capital growth can often be cost-prohibitive to get into and have yields so low that they can end up being negative after land tax is taken into consideration. The rent you receive isn’t even enough to cover the land tax on the asset in many cases. On the other hand, very high-yielding properties are usually found in very sparsely populated regional areas. The capital growth on these is often negative – if not in nominal terms then almost certainly in inflation-adjusted terms.

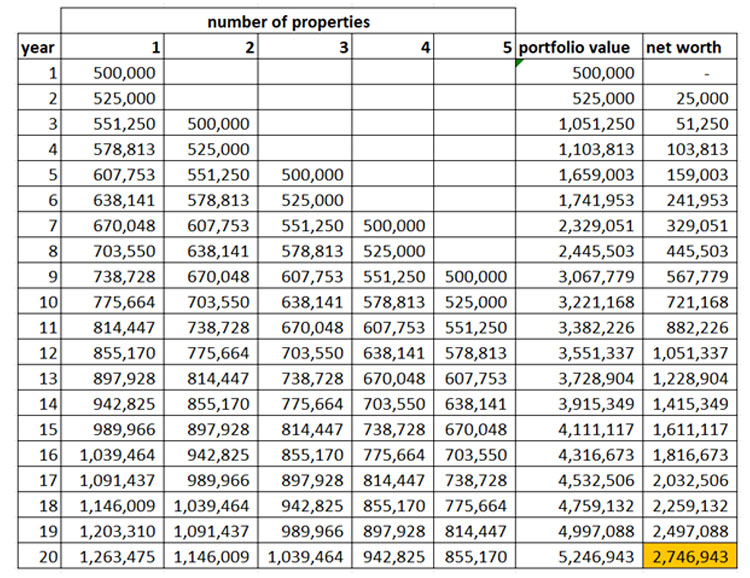

A typical strategy would be to use a higher growth type property yielding say 3.5 to 4% to build up the maximum capital we can over the course of our working lives. Then either stay with those properties if the rental income is high enough or sell them down and redeploy the capital into a property with a higher yield when it comes time to retire. Let’s have a look at a few scenarios. To keep things simple, we will assume each property is worth $500,000, the capital growth rate is 5%, the rental yield is 4.2% and you add another property to your portfolio every second year until you have a portfolio of five properties.

We can see that after 20 years the portfolio is now worth $5.2m and the net worth of your portfolio (which is the value of the properties less what you owe to the bank) is now $2.7m (highlighted in orange).

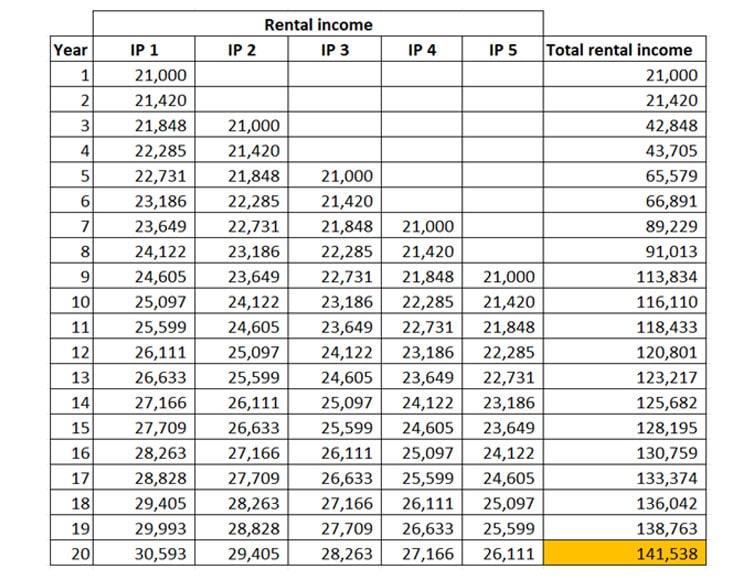

Your rental income would be as follows (assuming rents increased at 2% per annum)

Although the total rental income for all five investment properties would be a very respectable $141,530 per annum. Part of that is still going towards servicing the $2.5m in debt. If you were to sell down part of your portfolio and become debt-free your rental income would drop to around $60,000 per annum.

Let’s see what would happen if we liquidated the entire portfolio and redeployed the capital into a property portfolio that had a rental return of 6%.

If we were to sell down the portfolio and pay off the debt we would have $2,746,943. We would incur a 22.5% in capital gains tax on this leaving us with $1,566,381 in cash.

if we used this to buy a portfolio yielding 6% we would incur purchase costs of around 6% (primarily in stamp duty) leaving us with a portfolio worth $1,472,398 with a gross annual rental income of $88,348.

So we can see that even though the transaction costs such as stamp duty and capital gains taxes are high it can often be better to wear those and redeploy your capital into an asset with characteristics better suited to your stage in life… And one property isn’t going to be enough.