Please fill out the details below to receive information on Blue Wealth Events

"*" indicates required fields

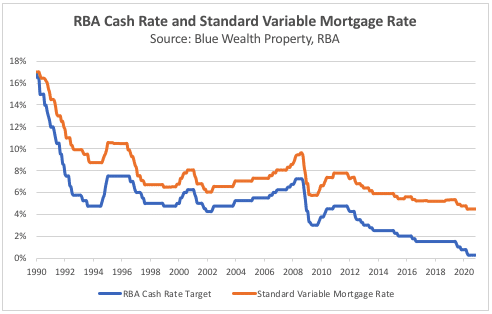

As you’ve probably heard, the RBA once again cut the cash rate target last week. It is now at an all new low of 0.1 percent. To put this into perspective, the RBA set the cash rate target two days before I was born (25 January 1990) at a whopping 17 percent. The early 90s saw it fall to single digits, where it bounced around until the aftermath of the GFC. Since 2011, it has steadily decreased from 4.75 percent to its current level.

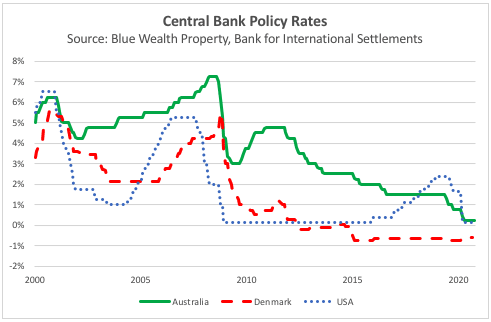

Australia’s cash rate decline accompanies many other economies around the world including the United States, Europe, United Kingdom, Japan and many more. In some of these countries, heated debate has emerged around the issue of negative interest rates… but what exactly does that mean? That lenders are paying borrowers interest instead of the other way around..? This week’s research blog uncovers this issue in more detail.

First, what is the RBA cash rate target?

Aside from filling your inbox with spam on the first Tuesday of each month, the RBA cash rate target serves various other purposes. Principally, its role is to determine the ideal interest rate on overnight loans between banks. Banks lend to each other over such short terms in order to meet their liquidity and regulatory requirements. This allows their customers to confidently withdraw cash if and when needed.

The function of the cash rate you’re probably more familiar with is its relationship with other interest rates. Whenever there is speculation surrounding cash rate changes, there is usually also speculation about how likely lenders are to pass on the change and how long it will take them to do so. Lenders can be sneaky and wait weeks or even months to pass on rate cuts if they do so at all. You’ve likely experienced this with your own lender at some point over the last few years. Particularly because the gap between the cash rate and standard variable mortgage interest rates is the largest it’s been since 1992 (according to RBA data).

Decreasing the cash rate to zero and beyond

You may have also noticed that decreasing the cash rate typically also decreases the interest you’re earning on your savings. It is therefore a way of discouraging savings, thus encouraging people and businesses to spend and borrow money which in turn stimulates the economy. When it comes to a negative cash rate, banks are incentivised to borrow from other banks with the prospect of paying back less than they borrowed.

Before you get too excited about your mortgage, keep in mind the gap between the cash rate and mortgage interest rates. Given the current gap, the cash rate would have to decrease from 0.1 percent to negative 4.27 percent or lower to reach negative mortgage interest territory. This is highly unlikely, particularly given the RBA governor’s stance. Nevertheless, negative mortgage interest rates are not unprecedented. Denmark is said to be the country most familiar with negative interest rates—over a period almost spanning a decade. This has prompted Danish lenders to offer negative interest rate mortgages, with the rationale being that they’d prefer to lose a little bit of money than lose a lot by charging a rate that customers cannot afford.

With limited data on the impacts of negative interest rates, it’s no surprise the RBA is apprehensive about taking this step. Instead, it looks like they’re focused on buying government bonds (lending money to the government). This is known as quantitative easing or more colloquially as printing money.

If the RBA had a change of heart and ventured into the realm of negative interest rates, we could expect a few things to take place. At a consumer level, savers would be compelled to invest in higher-return assets such as shares and property which will increase demand for these assets. Since the loans on these assets are cheaper, it is also likely we will borrow more. Although that could help the economy recover from the pandemic, we will have to be mindful of where asset prices and values are deviating from one another. In the case of residential real estate, history tells us this would most likely take place in Sydney.