Please fill out the details below to receive information on Blue Wealth Events

"*" indicates required fields

When I saw the impressively low numbers of coronavirus in Australia, I was pleasantly surprised. We Australians aren’t known for our adherence to rules, even if it means preserving our lives. Low and behold, a series of quite significant social distancing contraventions have since led to a second spike. Fortunately, by global standards, Australia is still doing extremely well. In fact, Australia’s current death toll is equal to about three days’ worth of COVID-related deaths in the United Kingdom. With the Victoria-induced second spike surpassing the country’s first, let’s hope the worst is now behind us.

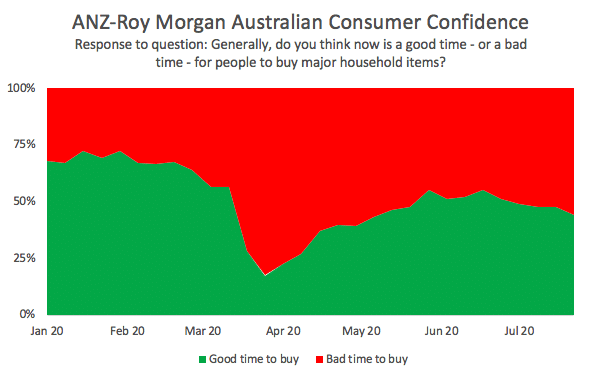

During these unique times, you may have noticed an increased use of shorter-term data than usual. One helpful weekly resource we have referred to during the pandemic has been the ANZ-Roy Morgan Consumer Confidence Index. Throughout the pandemic, this data tells us consumer confidence really fell off a cliff in mid-March. It then progressively recovered as we adapted to the regularly-cited new normal, but our reversal of COVID fortune in July prompted responses of lower confidence—just nowhere near the levels of the first spike.

Consumer confidence indexes are useful for property researchers because they offer a glimpse into the likely short-term purchase decisions of consumers. A portion of those individuals will also be homeowners and home buyers. Another weekly metric that gives some indication of the market is the auction clearance rate—something else that has been referenced quite a lot since the pandemic descended upon us. According to Domain, Sydney’s auction clearance rate was 65 percent last weekend, contrasting with 71 percent from the same time last year. Melbourne reported a figure of 58 percent, down from 74 percent from a year prior.

Auction clearance rates can be misleading. They only report on the percentage of homes up for auction which achieved a sale. What’s often neglected is the quantity of homes sold. Earlier in the year we made an obvious forecast that the total quantity of home sales would decline in the face of coronavirus. This turned out to be the case, with the first quarter of the year reporting less sales than at any other time since the Australian Bureau of Statistics began taking records in 2002. We certainly expect this trend to have continued in the second quarter, since the entire period was consumed by coronavirus. However, since consumer sentiment was on the mend over that period, it is very possible that the market readjusted to a new way of doing business.

Six months on from the emergence of coronavirus, we are still yet to see the substantial nationwide corrections forecast by some property pundits. Initially, the excuse was that the pre-COVID settlements needed to work their way through the system. Now that’s well behind us, there is still little evidence of a crash. One factor contributing to this is that the industries impacted most by job losses (hospitality, retail, etc.) have a low proportion of homeowners and investors. In addition, market interventions protected jobs and offered economic stimulus. Consequentially, we have actually seen growth figures in areas such as regional Victoria and certain postcodes within our cities.