Please fill out the details below to receive information on Blue Wealth Events

"*" indicates required fields

We have discussed houses versus units repeatedly since the founding of Blue Wealth Property… but with talking heads heralding the end of higher-density living since the onset of the pandemic nearly two years ago, what has changed..?

When the pandemic arrived in 2020, we were flooded with speculation of mass city exoduses—often fuelled by commentators selling investment properties in regional areas. What added to the confusion was that, in fact, our cities were losing people to regional areas (with the exception of Brisbane). If you stopped the conversation there, you could say the talking heads were right.

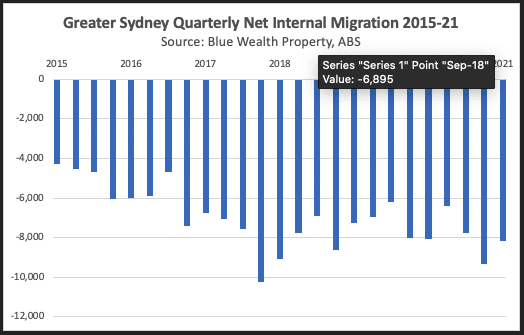

…HOWEVER, the conversation doesn’t stop there. As we have always known, our major capitals (especially Sydney) usually experience significant levels of negative internal migration (people relocating from one Australian area to another). Sydney’s population has only managed to grow due to overseas migration. In fact, Sydney hasn’t had a positive internal migration figure since ABS records began two decades ago.

Did COVID accelerate internal migration?

Although Sydney admittedly lost a net 31,564 people to internal migration in 2020, it lost 31,599 people to internal migration in 2017 and 38,410 in 2002. These three years don’t have pandemics in common. They have property booms in common.

Taking the above statistics into consideration, can we really say that Australians have fundamentally reconsidered our attitude toward higher-density urban lifestyles..?

What if we look at things from a different angle: the homes being built..?

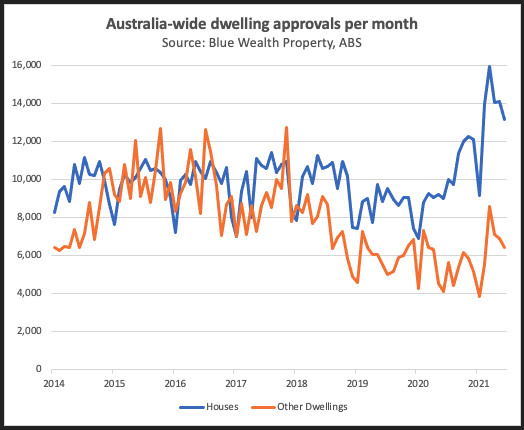

As you might be able to decipher from the squiggly mess below, something interesting happened at the beginning of the pandemic. In the first half of 2020, monthly house approvals increased by nearly 50 percent. Between February and June 2020, monthly approvals of ‘other dwellings’ fell by almost half. There’s no doubt that house approvals continued to skyrocket into early-2021, but ‘other dwellings’ managed to recover to pre-pandemic levels. Does the 2020-21 imbalance between houses and ‘other dwellings’ suggest a shift in preferences of Australians? I don’t think so. Instead, I’d point to the temporary first home buyer activity stimulated by government incentives (HomeBuilder) and record low interest rates.

…but how about the new work-from-home phenomenon? Won’t this solidify a reorientation to regional hubs and detached houses?

To answer this question, we need to indulge in a little psychology. More specifically, why do people live in cities in the first place?

This is a fun place for me to add a personal anecdote. When my wife, our dog and I left Australia in 2018, we had a vast range of destinations to choose from. I had secured remote work advising businesses and writing Blue Wealth’s series of eBooks which was enough to sustain a modest traveller lifestyle for the three of us (to begin with). What was our first destination of choice? Amsterdam. Why? It was well connected, had a vibrant culture, legendary nightlife, is picturesque, and the locals could speak good English. The problem? Rent was more expensive than Bondi. Why did we choose to burn through cash at a faster rate in Amsterdam than a provincial town elsewhere in the Netherlands? Because of the contrasts in lifestyle and amenity. Next, we moved to London, which enabled me to commence my studies at Oxford. We could have chosen any of the more affordable, cleaner and spacious ‘home counties’ closer to the university, but instead opted for an apartment within walking distance of London Bridge. When COVID hit, us and a number of friends took advantage of the temporary rental market discounts and upsized to a terraced house. There’s no doubt we lost some friends to the home counties, but many of them are making plans to return to the big smoke as life returns to normal here.

Of course, anecdotes do not necessarily reflect bigger picture trends, but this anecdote does go some way to explain why working from home doesn’t spell the end of higher density living. For thousands of years, cities have been a place where people converge, exchange and otherwise interact. The internet has facilitated a bit of flexibility in this regard, but the trade-offs don’t work for most people and organisations. This leads many experts to speculate on the proliferation of ‘hybrid’ working models, which means most workers will still be in the office at least one, two or three days per week. They’ll need an affordable home within a reasonable distance to work which also facilitates their lifestyle. For most city dwellers, that solution will continue to be an apartment.

But what do the numbers say..?

According to the CoreLogic home price index, units and houses across every capital city market experienced price growth in the 12 months to 31 July 2021. Over that period, houses outperformed units in the majority of capital city markets, but units had strong performance in markets where house prices were already reaching their limits. This reflects a similar dynamic to what we saw pre-COVID (reflective of the house-unit gap). In other words, houses continue to periodically experience higher rates of growth, but also bigger falls during market cooling. When it comes to rental performance, units still easily outperform houses in every capital city market.

| 12-month house and unit performance to July 2021 (select cities) Sources: Blue Wealth Property, CoreLogic, SQM Research |

||||||||

| Sydney | Melbourne | Brisbane | Hobart | |||||

| H | U | H | U | H | U | H | U | |

| 12m growth | 22.98% | 7.58% | 12.34% | 5.86% | 19.04% | 11.04% | 21.66% | 23.05% |

| Gross yield | 2.3% | 3.5% | 2.5% | 3.4% | 3.7% | 5.2% | 3.7% | 4.9% |

| Total 12m return | 25.28% | 11.08% | 14.84% | 9.26% | 22.74% | 16.24% | 25.36% | 27.95% |