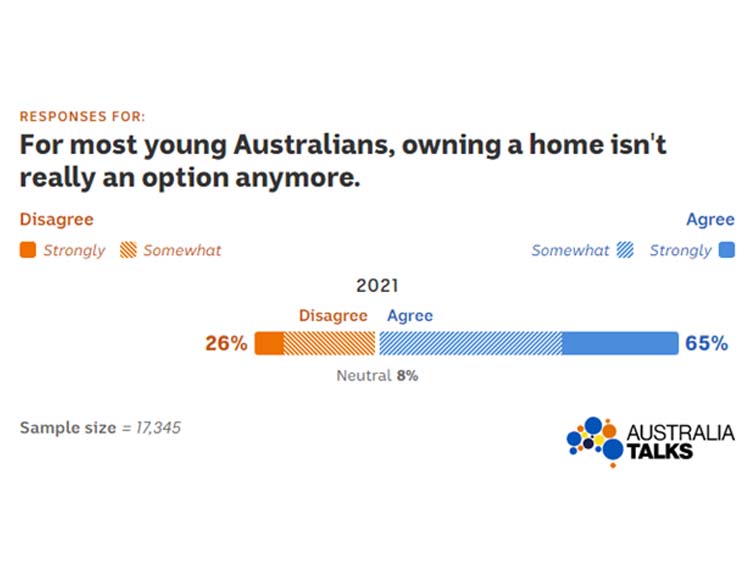

With home ownership being increasingly out of reach for Australia’s younger generation, it’s no wonder that 65 percent of Australians believe owning a home is no longer a choice for most young people (The Australia Talks national survey).

House prices have soared across Australia this year. Interest rates are low, market sentiment is high, people are spending less because of COVID-19 and a lot of these savings are finding their way into the property market. So, with home affordability becoming a major concern for our younger generations, should they commit to a mortgage and buy or continue to rent? The good news is that renting doesn’t mean you can’t own property as well. Let’s compare the options.

Buying

Owning your own home brings intangible benefits, such as a sense of stability, belonging to a community, and pride of ownership. At the other end of the spectrum, the overall cost of home ownership tends to be higher than renting. So, here are the pros and cons of buying your own home.

Pros:

It offers you security and freedom – Purchasing a home gives you peace of mind because you are not at risk of being evicted by a landlord. You also have the freedom to renovate and design your home as you wish.

House price appreciation over time – Owning an asset that will appreciate in price over time is desirable.

Being able to use the equity in your home – Provided that the value of your house is increasing, your equity will also increase as you pay off your loan. You may then be able to use the equity to invest in other assets – such as another investment property.

Cons:

You’ll be paying interest – the interest and fees you pay over the life of a loan can be significant and are not tax deductible. So in effect you could be paying twice the cost of your home after the interest expense is factored in.

There are opportunity costs — the cost of having your money locked up in real estate when it could have been used or invested elsewhere. If you opt for a life of renting, you’ll be able to use the money you’d have saved for a deposit and mortgage payments into something else, such as travel.

Ownership costs are more than just a deposit and loan repayments – There are significant transaction costs when it comes to buying and selling your property, there are additional costs such as agents fees and advertising. And about 6% of the purchase cost is spent on stamp duty, government fees, conveyancing costs, loan establishment fees.

Rentvesting

Contrary to popular belief renting doesn’t mean you can’t have any exposure to the property market. The word ‘Rentvestor’ has started to become a common term in the property industry. A Rentvestor is simply someone that rents in their dream suburb and invests somewhere they can make the best returns.

Living where you want to live – one of the massive benefits of renting is renting in a suburb that you want to live in.

Affordability – depending on your rent and the area you live; it is typically cheaper than mortgage repayments. Also, if you share a place with a housemate, you can split the rent, making it more affordable to rent rather than buy a home.

Investing – frees up cashflow which you could use for investments. You could use the spare cashflow to fund a portfolio of investment properties. In addition, the rent and tax savings from the investment property make it significantly cheaper to hold each property meaning you can control a much larger portfolio for the same outlay. For many investors in the current environment, it costs nothing at all to hold a property portfolio.

Cons:

Ownership – not owning the property can be a downfall as you don’t have a say if the landlord increases the rent or asks you to vacate the property.

Losing FHOG – if you’re a first home buyer, buying an investment property will lose you access to the First Home Owners Grant.

Capital gains tax – investments are subject to capital gains tax should you sell – unlike an owner-occupied residence where CGT does not apply. However, you will get a 50% concession on your CGT if you hold the property for longer than a year.

There is no right or wrong way of going about your property journey. If you want to learn a little bit more about this topic, click here.