Please fill out the details below to receive information on Blue Wealth Events

"*" indicates required fields

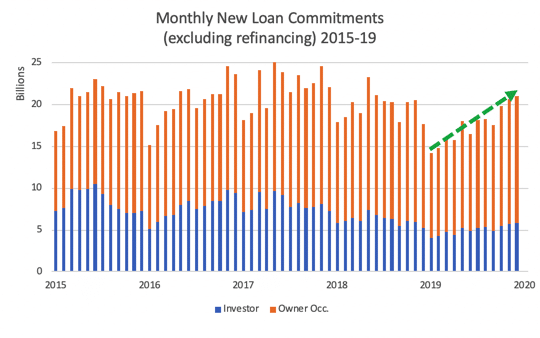

Last week, the Australian Bureau of Statistics (ABS) released updated figures of monthly new housing loan commitments. Figures have continued to trend upward since a six-year low was reached in January 2019. Over the course of 2019, occurrences such as a federal election upset, reserve bank rate cuts and revised regulatory conditions have markedly improved property market sentiment in many parts of Australia. The amount of money borrowed for new home loans in December 2019 was resultantly 49 percent higher than the January 2019 trough.

Levels of new housing finance are still below the record high of $25.3 billion in May 2017, largely due to the significant difference in the amount of finance being offered to investors. It is likely this figure will climb in 2020 as momentum grows, and potential market entrants begin to fear missing out on the forecasted upswing. Last week we cautioned investors caught up too heavily in the behaviour of others and reminded them to continue a commitment to buying in areas with strong longer-term fundamentals such as affordability.

As part of the 2019 “Triple Treat” of market shifts, the 10 percent annual growth cap on investor lending imposed on lenders by the Australian Prudential Regulation Authority (APRA) was lifted. In large part, APRA was reassured that tighter serviceability criteria imposed by lenders removed that risk from the market. Borrowing money today will therefore likely be more difficult than it was prior to the beginning of APRA’s interventions in 2015, but much more straightforward than it had been during the squeeze of 2015-19.

A stable resurgence of investor lending is something we welcome, as it promotes sustainable investment behaviour and goes some way to prevent overzealous market hysteria in the form we saw around Sydney’s peak in 2017. To open the floodgates all at once would be in few peoples’ interests, except perhaps the bankers.