The risks of property investment, like that of any investment, are real. In the face of those risks, some of you will enter a cycle of procrastination, leaving potential opportunities by the wayside. Others will realise that the market presents opportunities and will heed Warren Buffet’s words when he said ‘be fearful when others are greedy. Be greedy when others are fearful.’ So, what are the risks we need to be mindful of?

Oversupply

If the property market was an American high school movie, then oversupply would be the cheerleader. Rarely a headline is printed that doesn’t refer to the supply risk of our capital cities. It goes without saying that the combination of low interest rates and pent up demand have led to a rise in residential construction that’s seen the real-estate sector approach the contribution of mining to Gross Domestic Product. However, with rising construction costs and increasingly stringent lending policy, the feasibility of some approved projects is already questionable. In fact, The Financial Review reported that approximately 30% of approvals are unlikely to come to life. This doesn’t mean that supply risk isn’t real; projected supply in some regions, particular around our capital cities will likely leave demand playing catch up for a number of months. However, supply risk depends almost exclusively on the quality and value of the asset you’re investing in.

Timing Risks

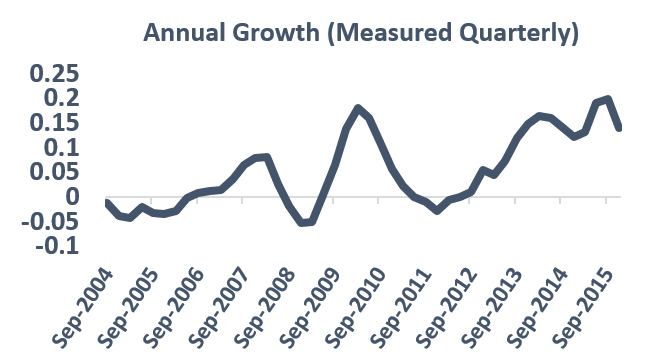

Property markets move in cycles. What investors need to be aware of is that the market cycles of our capital cities, or even suburbs within those cities, don’t necessarily align. This leaves opportunities to be exploited and risks to be avoided at any point in time. Where are those risks most acute? Falling markets like Darwin and Perth, and the affordability strained Sydney. Knowing where a property market is in its cycle is the key to mitigating timing risks. Here’s a look at where Sydney was placed as at September 2015:

Regulatory Risks

From a regulatory and lending perspective, there are three key points to be mindful of:

Loan to Valuation Ratio (LVR)

The LVR is the maximum loan attainable for a given property price. The ratio depends on a number of factors, most notably the risk assigned to the location in which you’re investing and your personal default risk. In some Australian suburbs, a high proportion of which are in Sydney, banks have reduced LVRs (i.e. you can’t borrow as much) to mitigate the risk of a market correction. We’ve long advocated a responsible investing philosophy and we welcome changes that increase the stability of the market.

Interest Rates

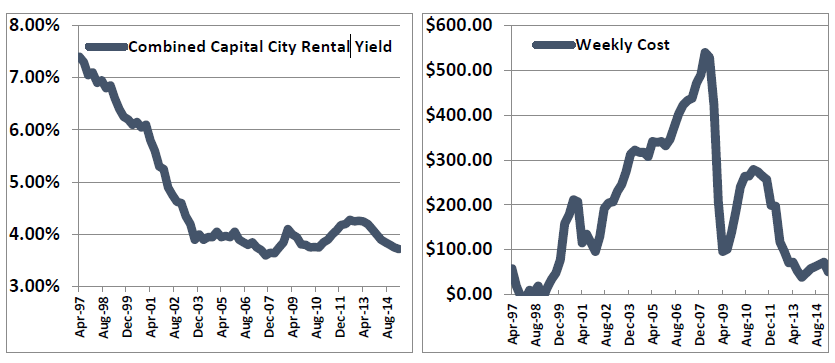

Macquarie Bank and Morgan Stanley analysts are predicting the RBA will cut the cash rate to 1% by the second half of 2017. This is largely in line with what the interbank cash rate yield curves tells us (click HERE for more information). What this means is that we’ll likely be in a low holding cost environment for at least the next few years. Check out how holding costs have evolved over the past couple of decades:

SMSF and Investor Lending

In July 2015, the Australian Prudential Regulation Authority (APRA) introduced a cap of 10% annual growth for a bank’s investment loan book. Why? The property market (particularly that of Sydney) was increasingly being seen as driven by investors rather than economic fundamentals. Some banks responded by increasing rates on investment loans, a step that, in some cases at least, has been reversed in the last ten months. Others responded to APRA’s announcement by restricting funding to self-managed super funds (SMSFs), or enforcing more stringent LVR conditions. For anyone with an interest in the long term stability of the property market, this is welcomed news.

Where to from here? You have two choices; procrastinate or act. I know what I’ll be doing.