Please fill out the details below to receive information on Blue Wealth Events

"*" indicates required fields

Exaggerated claims of detrimental market movements have been ringing through our airways for the last 24 months. Since our natural market correction in mid 2017, major household media influencers have rung the property bubble bell once again, urging many around the country to call for concern. I wanted to take a couple of minutes to look back and explain why recent housing performance is normal and a part of our nation’s natural economy. The reality is that recent results from our housing market are far from unique. Fundamentals remain strong opportunity for investment perpetuates.

Australia is a big country and our property markets that are fundamentally different. Whether it be economic drivers, median prices or general location – there are major variances between our housing markets that just can’t be ignored. As a result, measuring the movements of our national housing median is often an unhelpful way to get a clear analysis of market booms and busts.

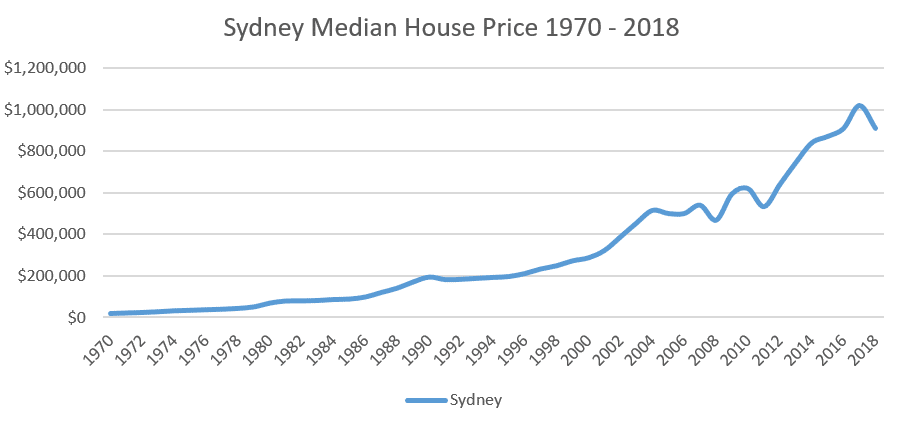

For the purposes of analysing ups and downs, were going to take a property 101 class on Australia’s most hotly-discussed property market: Sydney. Since 1970 Sydney’s median house price has grown to 50 times what it was. Over that period of time, there have been five instances when the median house price at the end of the year was lower than 12 months prior. What were the conditions that led to these situations?

Source: Australian Bureau of Statistics and Blue Wealth Property

1991: The two years that spanned 1990 and 1991 saw the RBA cash rate plummet from 17.5% to 8.5%. This era is now infamously known as Paul Keating’s ‘recession we had to have’. Sydney’s median house price recovered to the 1990 level by 1995.

2005: Sydney’s median house price experienced a $15,000 correction in 2005 but had recovered by 2007. Australia’s other three major cities (Melbourne, Brisbane and Perth) did not experience a price correction over this period. In fact, Perth’s median house price grew by $140,000.

2008: The year of the Global Financial Crisis. During this volatile period, lending was tightened and the number of house sales plummeted. The major agent for change here was the shift in the availability of credit which strained the volume of property sales around the country.

2011: This year was coined by some as the double-dip recession. In terms of Sydney property prices, this was the case. Median price drops lead many home owners and investors to offload their assets in fears that the market was so heavily inflated it could not improve. The subsequent recovery would lead Sydney into its most recent boom.

2018: After government slowing foreign investment with levies, banks tightening credit and federal politicians debating property taxes, the Sydney boom cools off and leads into a market correction phase. Again, major change here has been a slowdown in the amount of credit available and a dampening in market sentiment – both factors that are beginning to loosen.

Our property markets are resilient, its been proven time and time again. If you want to provide yourself with the best opportunity for growth, don’t rely on the headlines to educate yourself. Get into Blue Wealth today and get educated.