Please fill out the details below to receive information on Blue Wealth Events

"*" indicates required fields

Australia’s lending environment has been a rapidly shifting landscape over the past four years. While cash rates have come to an all-time low, APRA have initiated various restrictions to cool Sydney’s strongly performing housing market. The banking watchdog introduced new prudency restrictions in 2014, reducing the growth of investment loans to 10% per annum. Effectively, these actions encouraged new lending guidelines for banks, which has left some hopeful borrowers unable to secure finance. The big four banks (NAB, CBA, ANZ and Westpac) were forced to include limitations on serviceability, giving borrowers new hurdles to clear in hopes of securing loans – leading home buyers and property investors alike with the question:

Are banks still lending?

The reality is, banks and non-bank institutions are still lending (it is their main source of income) but you may require a financial professional’s aid to successfully navigate the new lending landscape. If you asked anyone braving the lending environment on their own this question, they would probably tell you no. This portion of borrowers would have found the market exceedingly difficult to navigate without insider knowledge.

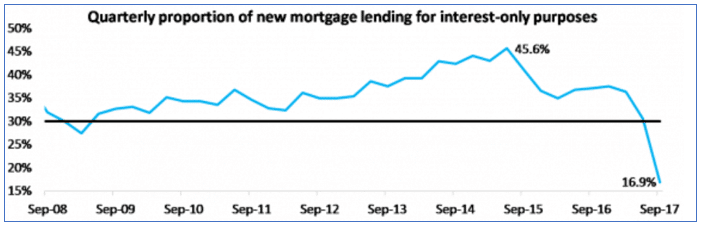

Recently, the portion of interest only lending dispersed by banks has tapered downward. In the Quarter 3, 2017 only 16.9% of new mortgages were interest only loans, down from 33.9% in the previous year. The reality is that the demographic securing interest only loans are either in a strong financial position or, are assisted by a broker’s expertise – not that banks “just aren’t lending”.

Source: CoreLogic

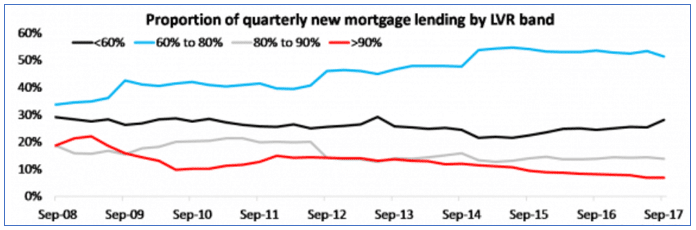

Reports from CoreLogic indicate that there has also been a drop in the lending of high loan to value ratio loans. The number of mortgages that have an LVR of 90% or above have dropped by 13.3% in the twelve months to September 2017. These numbers depict how prudent much of the banking sector has become of recent times, even those who have been able to secure a 10% deposit will have faced some hurdles to borrow.

Source: CoreLogic

Circumstances, however, are beginning to turn. APRA has realised the impact of these limitations, which seem to have run their course. In the words of APRA chairman Wayne Byres the restrictions have ‘served their purpose’, after the decision to relax the cap on investor loan growth as of June 1st, 2018. Meaning banks will look to increase the amount of investment loans over the midterm. In terms of property investment this may mark an opportunity for borrowers within a re-calibrating market, as lending will be increasingly available to those who seeking interest only and investor loans.

Borrowers may start to look at the market with more optimism over the next two quarters. There lies an opportunity as lenders may start to offer favorable deals to gain competitive advantage in a looming market. Lenders may offer deals in the form of lower rates and more favourable conditions, in attempt to catch rising demand from investors as the market begins to flow more freely. Often this type of competition throughout a lending cycle will spur lenders to top each other. It is in lending environments such as these that a broker’s advice benefit investors heavily.

In addition to lending becoming more accessible over the short term, holding a property remains relatively cheap. Low interest rates and strong rental returns have made it progressively easier to cover the costs of investing, with the current conditions creating an economical market for potential buyers. In current circumstances it costs as little as $40 dollars per week to hold a $500,000 property.

It seems the lending environment is set to shift again over the midterm, possibly in favour of the borrower. The upcoming legislative reforms mark changes in bank lending that will create a stronger position for investors. It is in this environment that buyers should seek the skill set of their finance professionals to understand the market. Obtaining the knowledge of an expert that knows how to appreciate and navigate lenders can mean the difference between good or bad finance outcomes.